Recently, there have been increasing reports in the media about changes regarding the tax obligations of property owners renting privately. Although many of these regulations primarily concern VAT taxpayers, the changes may also affect those who currently benefit from exemptions. Below we present what is worth knowing and how to prepare.

1. Property Owner as a VAT Taxpayer

According to the regulations, a person renting out a property – even within the framework of private rental – acquires the status of a VAT taxpayer (although often this is an exempt entity).

• In practice, private rental for residential purposes benefits from an exemption (Article 43(1) of the VAT Act) — which means that this service is exempt from VAT and the owner does not have to issue an invoice unless the tenant (e.g., a company) requests a document.

• There is also an exemption based on the entity — when the income from activities (including rental) does not exceed a specified limit (until the end of 2025, 200,000 zł, later 240,000 zł) — then the owner does not become an active VAT taxpayer.

• If the owner is an active VAT taxpayer and rents the property to a company (B2B), they are obliged to issue an invoice in accordance with VAT regulations.

These rules are currently in effect — however, starting in 2026, there will be a key change in the form of the obligation to use the KSeF system (National e-Invoice System), which may also affect owners benefiting from exemptions.

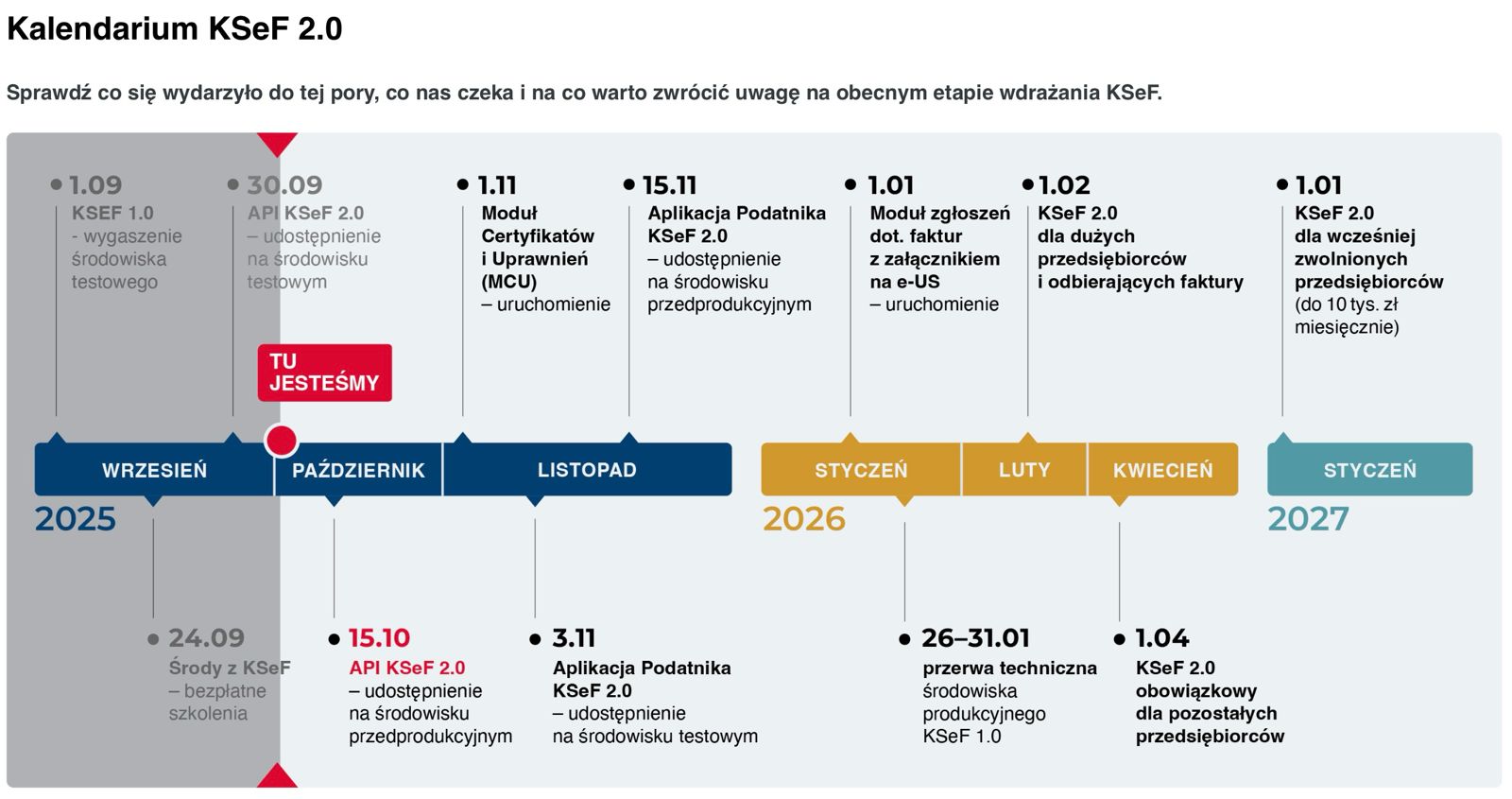

2. KSeF (e-invoices) – New Mandatory Framework

KSeF is a central electronic system handling structured invoices. Until now, many people believed that these changes did not concern them, but the situation is beginning to change.

Main deadlines and scope:

• The obligation to receive invoices through KSeF will apply to all taxpayers starting from February 1, 2026.

• The obligation to issue invoices through KSeF will cover other taxpayers from April 1, 2026, including those renting properties.

• Micro-taxpayers issuing low-value invoices (gross ≤ 10,000 zł per month) may have a transitional period (or exemption) in the first year of implementation, although this mainly concerns sales, not rentals.

What does this mean in practice:

• Even owners currently exempt from VAT will have to use KSeF if they issue invoices (e.g., for companies).

• In the case of rental to an individual (B2C): personal invoices (or receipts) will not be subject to mandatory KSeF — the owner can issue a document outside the system if the tenant requests it.

• If the owner does not have a NIP number (and has been settling on PESEL), to issue an invoice through KSeF for a B2B tenant, they will need to obtain a NIP.

• Regarding cost invoices (e.g., utilities) – when suppliers will use KSeF, to receive such an invoice, the owner must be visible in the system as an exempt VAT taxpayer.

3. Practical Scenarios – What You Need to Know as an Owner

Scenario A: private rental (B2C), apartment for residential purposes

• Most often, you benefit from the subject exemption — you do not have to issue an invoice or use KSeF.

• If the tenant (individual) requests a document — you can issue a regular receipt or personal invoice outside KSeF (until the system becomes mandatory).

• When the KSeF obligation for issuing invoices (for B2C) comes into effect — this case will be covered by statutory exceptions.

Scenario B: rental for a company (B2B)

• If you are an active VAT taxpayer: you issue invoices, preferably with immediate integration with KSeF.

• If you benefit from the entity exemption: until 2026 you do not have to issue invoices, but when the tenant requests a document — it must be issued through KSeF.

• In practice — from April 1, 2026, property owners B2B will have to use the system.

Scenario C: issuing cost invoices (utilities, services)

• Dos